Share the Rewards. As a member-owned captive, Wildcat empowers businesses to manage risk, reduce volatility, and build lasting financial strength together.

Strength in Shared Ownership.

Wildcat brings together like-minded companies to gain control,transparency, and long-term stability in their insurance programs.

Take Control. Gain Peace of Mind.

Eliminate the mystique of the insurance industry. Through ownership in Wildcat, members gain the transparency and expertise needed to make insurance a predictable, manageable cost.

Stability in a Volatile World.

Wildcat is more than an insurer, it’s a robust company built on a long tradition of owner-managed performance and risk-management success.

Take Control. Gain Stability.

Share the Rewards. As a member-owned captive, Wildcat empowers businesses to manage risk, reduce volatility, and build lasting financial strength together.

Strength in Shared Ownership.

Wildcat brings together like-minded companies to gain control,transparency, and long-term stability in their insurance programs.

Take Control. Gain Peace of Mind.

Eliminate the mystique of the insurance industry. Through ownership in Wildcat, members gain the transparency and expertise needed to make insurance a predictable, manageable cost.

Stability in a Volatile World.

Wildcat is more than an insurer, it’s a robust company built on a long tradition of owner-managed performance and risk-management success.

Our

Captive

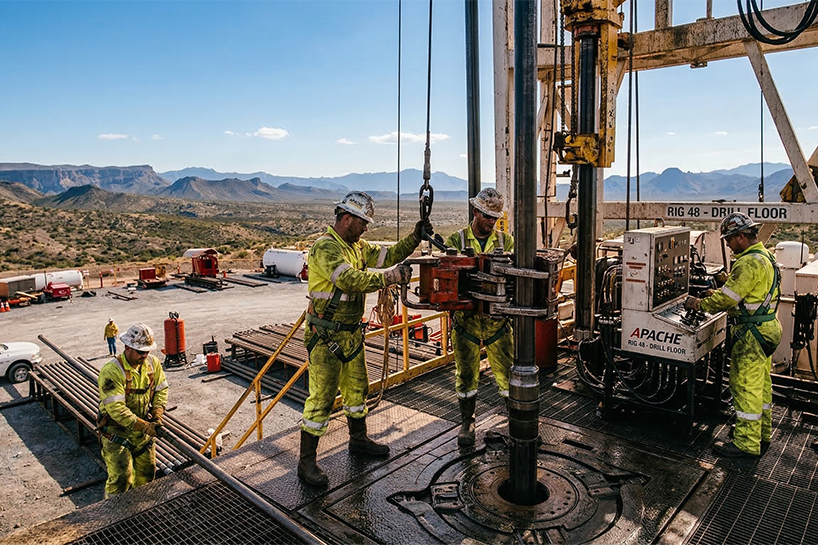

Wildcat Energy Insurance, Ltd. (Wildcat) is a member-owned group captive created to give upstream and midstream oil and gas companies, along with the renewable energy sector, a more customized, stable, and affordable insurance alternative. Built for above-average, safety-focused operators and service firms, Wildcat brings peers together across the energy value chain, from drilling and well servicing to construction, pressure pumping, and engineering, so members can reduce volatility, strengthen risk performance, and gain more control and transparency over their insurance program. Each shareholder has a voice in governance and benefits from the group’s shared commitment to safety and long-term stability, turning insurance into a smarter, more strategic advantage.

Wildcat Energy Insurance, Ltd. (Wildcat) is a member-owned group captive created to give upstream and midstream oil and gas companies, along with the renewable energy sector, a more customized, stable, and affordable insurance alternative. Built for above-average, safety-focused operators and service firms, Wildcat brings peers together across the energy value chain, from drilling and well servicing to construction, pressure pumping, and engineering, so members can reduce volatility, strengthen risk performance, and gain more control and transparency over their insurance program. Each shareholder has a voice in governance and benefits from the group’s shared commitment to safety and long-term stability, turning insurance into a smarter, more strategic advantage.

Member premiums are no longer directly tied to the unpredictable traditional market. In Wildcat, a members performance, not outside cycles, is the primary driver of its long-term insurance cost.

Experience true shared risk with full transparency into where every premium dollar goes, plus the opportunity to build equity and achieve powerful financial efficiencies.

Member premiums are no longer tied to the unpredictable traditional market. In Boulder, your business’s performance, not outside cycles, is the primary driver of your long-term insurance cost.

Experience true shared risk with full transparency into where every premium dollar goes, plus the opportunity to build equity and achieve powerful financial efficiencies.

“Since joining Wildcat in 2021, our premiums have stayed remarkably stable despite volatile markets. The expertise, transparency, and true partnership mindset we’ve experienced through Captive Resources have made a meaningful difference in managing our risk and controlling costs long-term.”

CFO/Safety Director

Joined 2021

“Our 14 years in Wildcat have been one of the best decisions we’ve ever made, financially and beyond. The connections we’ve built with other safety-focused companies are invaluable, and unlike traditional insurance, we have a real voice in how things are run. We’ve never felt like our hands are tied.”

President/CEO

Joined 2011

“Over more than a decade in Wildcat, we’ve realized meaningful financial benefits while gaining greater transparency and control over the complex risks in our industry. The program is run with a level of professionalism and discipline that simply sets it apart from the traditional insurance market.”

VP of Finance

Joined 2014

“Being part of Wildcat has given us stability in a volatile market, especially when it comes to auto insurance. The renewal process is efficient, the Captive Resources team is a pleasure to work with, and we can focus on running our business with real confidence.”

CEO

Joined 2020

Group Captive Insurance vs Traditional Insurance

Group Captive Insurance vs Traditional Insurance

Group Captive

Owning It Members share ownership and decision-making power.

Transparent Costs Premiums reflect your performance, not market swings.

Shared Rewards Investment income and profits stay with members.

Input Encouraged Have a voice in selecting service partners and participate in the claims process.

Stability Through Safety Strong risk management leads to predictable costs.

Traditional Insurance

Renting It The carrier controls decisions and keeps the profits.

Unpredictable Costs Premiums shift with industry trends, not results.

No Shared Returns Investment income benefits the carrier, not you.

Limited Input Claims and services are generally managed without your oversight.

Market Volatility Rates rise and fall regardless of your performance.

Group Captive

Owning It Members share ownership and decision-making power.

Transparent Costs Premiums reflect your performance, not market swings.

Shared Rewards Investment income and profits stay with members.

Input Encouraged Have a voice in selecting service partners and participate in the claims process.

Stability Through Safety Strong risk management leads to predictable costs.

Traditional Insurance

Renting It The carrier controls decisions and keeps the profits.

Unpredictable Costs Premiums shift with industry trends, not results.

No Shared Returns Investment income benefits the carrier, not you.

Limited Input Claims and services are generally managed without your oversight.

Market Volatility Rates rise and fall regardless of your performance.

What are the benefits of a captive insurance company?

The insurance marketplace has historically endured “hard and soft” market cycles where premiums go up and down with little relation to an actual loss experience. By pooling resources and becoming owners of an insurance company, these swings can be eliminated, making insurance costs not only more predictable but potentially profitable. This is achieved through unbundled services resulting in lower operating costs and the ability to retain investment income.

Is a member at financial risk by being in a captive?

If it is done properly, the company is not. If all the company were doing is each paying a premium into a fund in a bank and hoping the losses didn’t exceed the fund, then yes it would be risky. If, however, the program is structured properly, using a licensed admitted insurance company to act as the fronting company that issues the policy, and if we use a financially strong reinsurance company to insure the catastrophic losses, the risk is minimal. Under this concept, the assumption of risk occurs only in the smaller, predictable layer. By cutting operating costs and earning investment income, financial risk is reduced, and the bottom line is enhanced.

What loss control and claims handling service enhancements are provided by the captive that are not normally available in the traditional insurance marketplace?

The captive has a specialized loss control program administered by various risk control consultants. Claims are administered by Zurich. Special claim handling instructions are prepared for each member’s specific needs. Since Wildcat is capable of securing these services independently on an unbundled basis, members are assured that the service provider is evaluated based on the quality of its work product. In addition, Captive Resources in its advisory capacity assigns a member of its claims and risk control staff as a member advocate. Finally, Wildcat conducts two risk control workshops each year which allows for an exchange of information between members that is not possible in the conventional market.

How long do the insureds remain in the captive?

Insureds are committed to the captive for only one policy period. Profits are based upon the policy period in which the insured is a member. The captive does ask members to make a moral commitment for at least three years, to give the member an opportunity to learn and understand all of the workings of the captive.

Can members be assessed if the underwriting results do not turn out as planned?

The company’s loss exposure and its loss fund will be established by the captive’s independent actuary. Typically, any assessment will be driven by the company’s loss experience. Assessments are limited, and members should generally know their expected maximum amount upfront. That said, depending on circumstances, there could be risk of underwriting losses.

Is Wildcat a rent-a-captive?

Wildcat is not rent-a-captive arrangement. Unlike many other group captives, which are controlled and managed by brokers, and/or agents, this is a captive owned by shareholders, directed by the shareholders.

What coverages are underwritten in the insurance program?

The captive reinsures the carrier for Automobile Liability and Physical Damage, Workers’ Compensation, and General Liability including Products and Completed Operations of its members. Property coverage is available for all casualty members through another captive option.